Given the negativity that has ravaged the car industry this year, the Society of Motor Manufacturers and Traders’ (SMMT) commentary on the 4.4% drop in year-on-year UK new car registrations for September – traditionally the second-strongest month of the year, due to the plate change – was appropriately downbeat.

SMMT chief executive Mike Hawes underlined this mood, emphasising the worst September sales performance this century: “During a torrid year, the automotive industry has demonstrated incredible resilience, but this isn’t a recovery. Despite the boost of a new registration plate, new model introductions and attractive offers, this is still the poorest September since the two-plate system was introduced in 1999.”

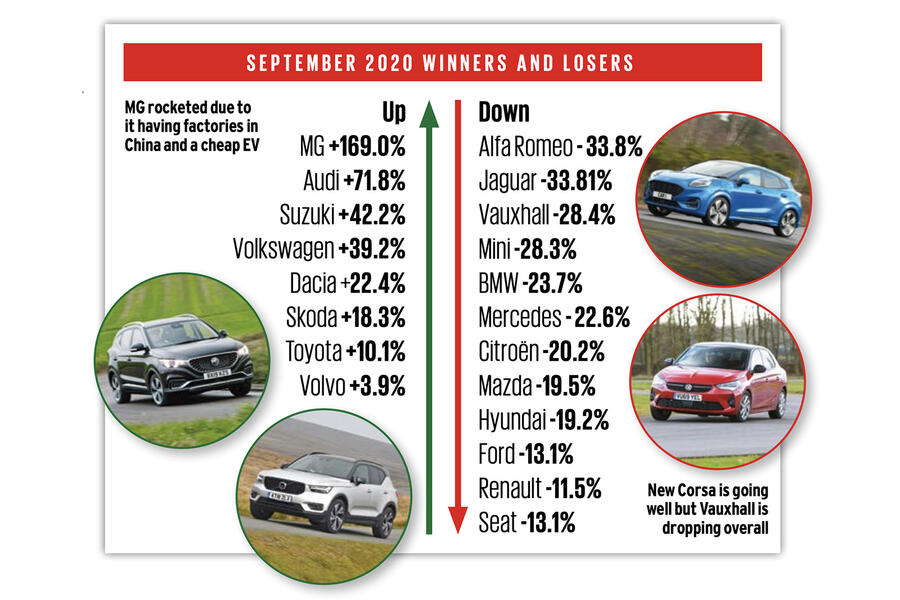

It was this position that led the national headlines, the bad news further exaggerated by the knowledge that September 2019 had itself been deemed extremely disappointing, due to some key manufacturers – led by Volkswagen Group brands – not having enough WLTP-emissions-compliant stock ready for customers.

The gloom was based on inarguable registrations data and backed by the prediction that the year will now end 30.6% down from 2019 – a fall of 708,000 units. That’s an estimated loss of £21.2 billion of sales based on industry analyst JATO Dynamics’ estimation that the average car in the UK is sold for £30,000.

However, the SMMT position tells only one side of the story. In total contrast, talking to a wide range of retail group leaders both on and off the record, Autocar received universal reports of a month of resounding sales success.

“Trading conditions were as strong as I can remember. For us at least, it was a record month for profitability, and it’s possibly the case for the industry as a whole, I would think,” said Robert Forrester. He’s the boss of Vertu Motors, the fifth-largest franchised dealer group in the UK, with more than 120 different outlets spanning mainstream and premium brands, as well as one of the largest commercial vehicle retailers in the UK.

Vertu’s interim reveal the scale of its success: private sales were up 6.3% year on year, Motability sales up 8% and new van sales up 53.3%.

John O’Hanlon, the chief executive of Waylands Automotive, a Volvo dealership group, reported new car sales up 70% year on year and used car sales up 30%, albeit out of expanded premises.

Additionally, he noted that aftersales profits were up 30% and parts sales profits were up 20% as people flooded back to get MOT test and servicing work done, adding further impetus to the retail recovery.